The following describes the functionality and features included in Probe Audit Premium+

Instructions:

10.20 - ENGAGEMENT EVALUATION

Watch the video for detailed guidance on the document above, then read the summary below for a concise overview.

Objective

The objective of this document is to ensure that the audit firm accepts and continues to accept clients and engagements that fit the firm's risk profile and that the terms of the engagement have been agreed upon between the firm and the client.

The following key concepts of the Probe Audit Premium+ Methodology are set in this document:

- Going concern consideration at the planning stage

- The possible impact of users of the financial statements

- Desired audit risk

Document placement

Document 10.20 – Engagement evaluation can be found in the Pre-engagement planning folder in the Caseware document manager.

Document content

This document is designed to be a questionnaire type document with space for a comment or further description.

This document is divided into different bookmarks in the document map to assist you in evaluating the engagement. The document map is responsive based on questions answered in the engagement file:

- Type of engagement

- Terms of the engagement

- Engagement acceptance or continuance

- Ethical requirements

- Going concern

- Users of the financial statements

- Conclusion

- Engagement partner declaration

Layout

|

COLUMN

|

INPUT REQUIRED

|

OUTCOME

|

|

Question

|

No input required in this column. Some questions may only be shown based on the answers to earlier questions.

|

No impact on the engagement file.

|

|

Yes/No

|

Answer the question by selecting from the "Yes / No" drop-down box.

|

By answering the questions your engagement file will be tailored and further relevant questions will be shown in the engagement file (or hidden if not relevant).

|

|

Description

|

Include a short description, if necessary, to substantiate or expand on the “Yes / No” answer selected.

|

No impact on the engagement file.

|

|

Risk

|

Raise a risk or event, if necessary, relating to the question or the responses reflected.

|

A risk or event will be recorded in the relevant document. The engagement file will then prompt the engagement team for appropriate responses to the risk or event recorded.

|

|

Ref.

|

If necessary, insert a reference to other documents in your engagement file.

|

No impact on the engagement file.

|

The following important questions/procedures are included in the document:

|

Question

|

Impact on the engagement file

|

|

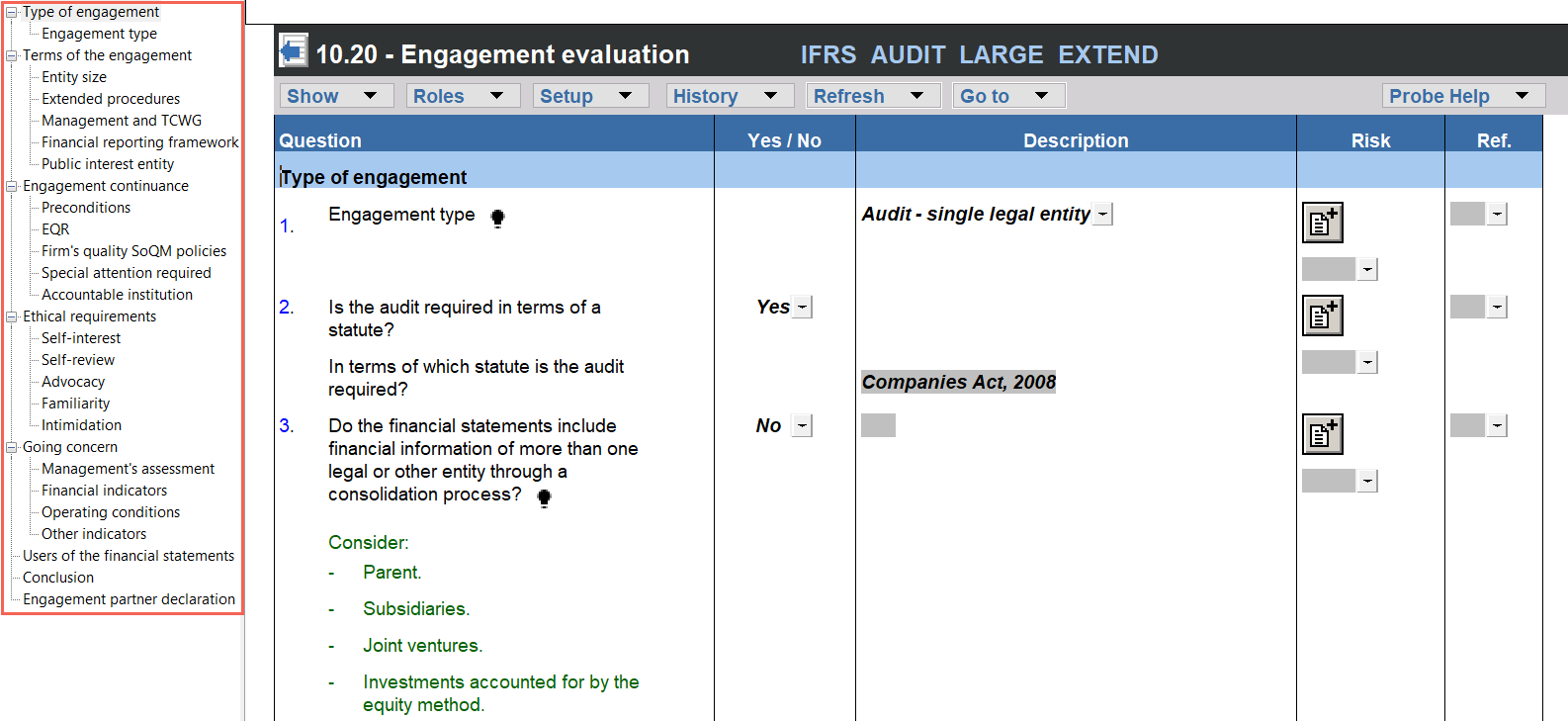

Engagement type

|

Selecting the relevant engagement type will amend the rest of the file according to your selection.

When selecting ‘audit’, the engagement file includes audit procedures for an audit engagement in terms of the International Standards on Auditing (ISAs).

When selecting ‘Review’, the engagement includes procedures to be performed in terms of ISRE 2400 (Revised) Engagements to Review Financial Statements.

When selecting Group Audit Single or Group Audit Multiple, the engagement file includes audit procedures to be performed by the group auditor in the capacity of group auditor in terms of ISA 600 (Revised), Special Considerations – Audits of Group Financial Statements (including the Work of Component Auditors)

|

|

Do we elect to use the extended procedures to assist the engagement team with gathering and considering relevant information?

|

Selecting ‘no’ will reflect core procedures only. The engagement file will therefore include the procedures based on the requirements of the ISAs.

Selecting ‘yes’ will reflect extended procedures, which includes the ISA requirements as well as additional audit procedures, questions and considerations based on the application and other explanatory material.

|

|

Does ‘Management’ include all of ‘Those Charged with Governance’?

|

Additional procedures, based on the ISAs, will be included related to those charged with governance when management and those charged with governance are different.

|

|

Financial reporting framework

|

Risk assessment and further audit procedures will be expanded to address specific recognition, measurement and disclosure requirements when the IFRS Accounting Standards or the IFRS for SMEs Accounting Standard is selected.

|

|

Is the entity a Public Interest Entity (PIE) as defined by the IRBA Code of Professional Conduct for Registered Auditors?

|

When the entity is a PIE, the engagement file will include additional documentation of considerations specifically applicable to PIEs.

The audit report will also include additional paragraphs, as applicable to PIEs.

|

|

Will key audit matters be presented in the audit report?

|

Selecting ‘yes’ will prompt users to consider Key Audit Matters identified during the prior period (10.50 Gathering information) and the engagement team will have to complete 02.55 – Key Audit Matters.

The audit report will also have to include information about Key Audit Matters.

|

|

Is this engagement subject to an engagement quality review (EQR) according to the firm’s System of Quality Management (SoQM) policies and procedures?

|

If the engagement is subject to an EQR, the engagement quality reviewer will have to review documentation in the engagement file and specifically complete 12.40 – Engagement Quality Review – Planning (Audit) and 02.80 – Engagement Quality Review – Execution and finalisation.

|

Document outcomes

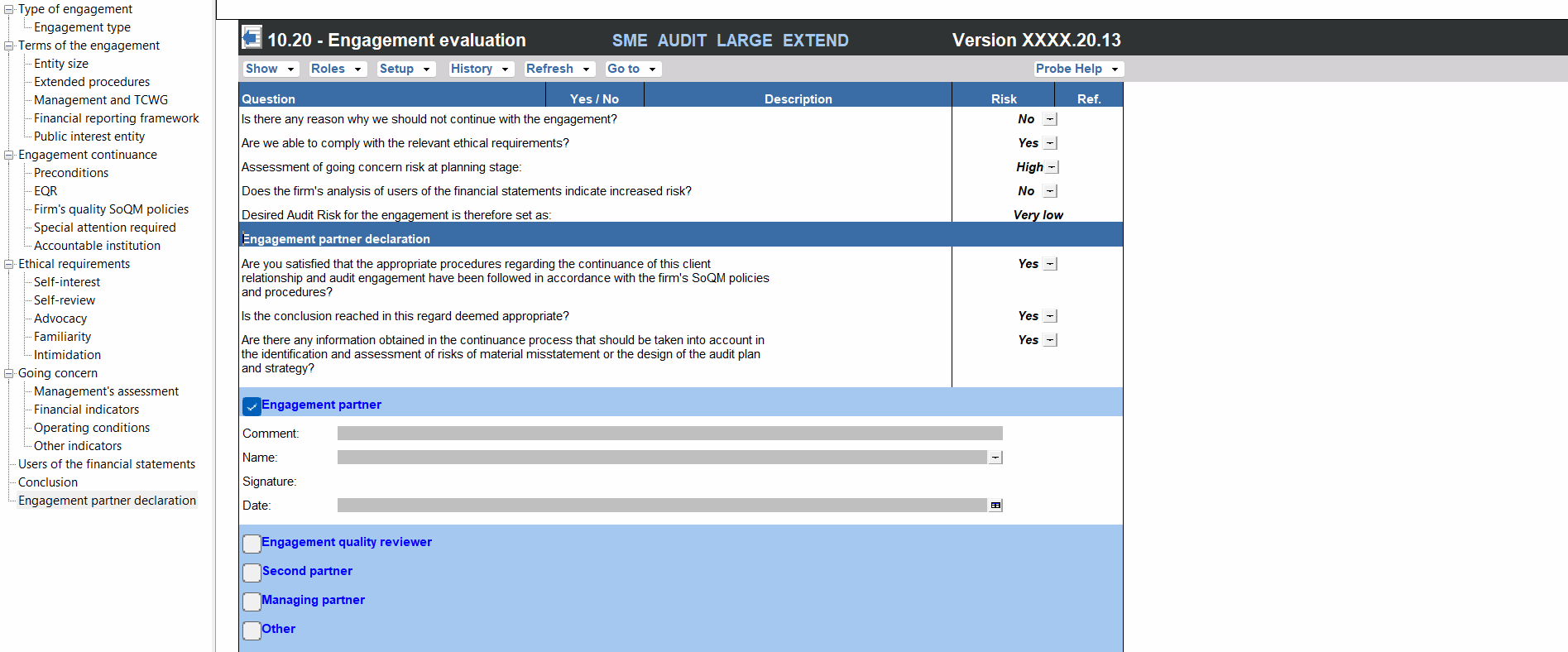

Overall outcomes

- You must reach a conclusion on the following items in this document:

- Whether or not the firm should continue with or accept the engagement;

- Whether or not the firm will be able to comply with the relevant ethical requirements;

- The assessment of the going concern risk at the planning stage;

- The risk posed by the use of the financial statements by external users; and

- The desired audit risk for the engagement.

Engagement partner declaration

The engagement partner declaration requires the engagement partner to conclude whether:

- the procedures for the acceptance or continuance of the client relationship and the audit engagement have been followed in accordance with the firm’s SoQM policies and procedures;

- the conclusion reached in this regard is deemed appropriate; and

- any information that has been obtained in the acceptance or continuance process should be taken into account in the identification and assessment of risks of material misstatement or the design of the audit plan and strategy.

The Engagement partner signs the document off. If an additional team member has been involved, e.g. a managing partner or EQR, you can provide space for their sign-off by selecting the relevant option. The descriptions for the additional partners can be changed in Probe Firm settings. It is assumed for a small engagement, that the firm will only have an engagement partner assigned to the audit.

Group audits

When the engagement type was selected as Group Audit Single or Group Audit Multiple, questions are modified for the separate group audit engagement file.

Additional questions were added for group audit engagement to:

- Identify components for planning and performing of audit procedures;

- Determine expected involvement of component auditors in risk assessment procedures and further audit procedures;

- Evaluate access to components and component auditors; and

- Determine whether there is any indication that the group auditor will not be able to be sufficiently and appropriately involved in the work of the component auditor.

Some questions include red warnings or blue text in the description column. Follow the red warnings that inform you where key information should be recorded and the blue text in the description column that advises you where the understanding may be documented.

Features

The following features are available in the document:

Insert or delete a comment, see page F3

Insert or delete a row at the end, see page F5

Record a risk or event, see page F10

Core vs Extended, see page F15

Guidance, see page F16

Freeze, see page F17

Rate this article:

|vote=None|

Processing...

(Popularity = 3/100, Rating = 0.0/5)

Related Articles

Compilation | 06.20 Compilation engagement evaluation

F23 | Probe | Select engagement

Probe Audit | 10.50G - Plan extent of risk assessment procedures

Probe Audit | Planning Risk Assessment | 11.50 Information system and control activities

view all...

Search Results

Editing the Company Registration Number

What is the client registration number?

XBRL Lite | Version number (IFRS) 2023.05.01, 2024.05.01 & (SME) 2023.04.01, 2024.04.01

Can my client signer give authorisation to multiple companies at the same time?

Editing Authorised Signer Details

view all...