Executive summary

This annual update of the IPSAS Financial Statements adds the latest effective IPSAS presentation and disclosure requirements from the IPSAS Standards to your IPSAS Caseware file. Notably there was no major changes in the effective IPSAS standards from 2024 to 2025. However, the far-reaching implications of IPSAS 41 and subsequent impact are still being unravelled. This release focusses on implementing these subsequent impacts on the financial statements which were not covered in the previous releases as well as implementing exiting localisation features requested by our clients.

This release will bring back the option to update your entire Caseware file or to only add the latest compliance changes, dependent that your Caseware file is on version IPSAS 2024.11.01.

This update coincides with the full market release of Caseware Working Papers (Version 2024.00.162) and Connector (Version 2024.00.003).

Contents

1. IPSAS 2024.11.02

1.1. IPSAS 41 (read together with IPSAS 1, IPSAS 29 and IPSAS 30)

1.1.1. Construction contracts and receivables

1.1.2. Finance lease receivables

1.1.3. Hedging

1.1.4. Fair value Information

1.2. IPSAS 3

1.3. Other minor improvements

1.4. User requests

2. Caseware Working Papers 2024.00.164

3. Previous release - IPSAS 2024.11.01

4. Previous - Caseware Working Papers 2024.00.092

1. IPSAS 2024.11.02

1.1. IPSAS 41 (read together with IPSAS 1, IPSAS 29 and IPSAS 30)

The following improvements are introduced based on the subsequent assessment of the impact of IPSAS 41 (read together with IPSAS 1, IPSAS 29 and IPSAS 30):

1.1.1. Construction contracts and receivables

- The impact of IPSAS 41 on IPSAS 11 was assessed and resulting in the following changes:

- Added under Non-current Assets on the Statement of financial position a new line item for Construction contract and receivable. [BS]

- Updated the Construction contract and receivable note with financial instruments related disclosures. [NOTES_018]

1.1.2. Finance lease receivables

- The impact of IPSAS 41 on IPSAS 13 was assessed and resulting in the following changes:

- Updated the Lease receivables note with financial instruments related disclosures. [NOTES_014]

1.1.3. Hedging

- Added a new note to assist with the disclosure required for Hedging and hedging instruments. [NOTES_258]

1.1.4. Fair value Information

- Added a new note to assist with the disclosure about Fair value Information. [NOTES_259]

1.2. IPSAS 3

Update the New standards and Interpretations note with the latest new IPSAS standards issued but not yet effective. [NOTES_047]

1.3. Other minor improvements

The following minor improvements are also introduced:

- Updated the correct reference to "Gain on reclassification of financial asset from amortised cost to fair value through surplus and deficit".

- Updated the correct reference to "At fair value through surplus and deficit".

- Updated the correct reference to " "FVSD" (fair value through net assets)".

- Updated the IPSAS reference on the Statement of Financial Position and Statement of Financial Performance.

1.4. User requests

The following users request features are now available in this update:

- Flexible headers for the period references at the top of the balance columns. Additional text can be added via the column settings in the Information store.

- Ability to insert a "Heading row" via the super insert feature.

2. Caseware Working Papers 2024.00.164

The following describes the features and fixes included in Working Papers 2024 and related products.

2.1. Features

2.1.1. Xero Online (Direct) Import

- Working Papers now fully supports imports from Xero Online. You can import your Xero trial balance and general ledger details from the Import - Accounting Software dialog without having any licencing errors using the “Xero Online(Direct)” option.

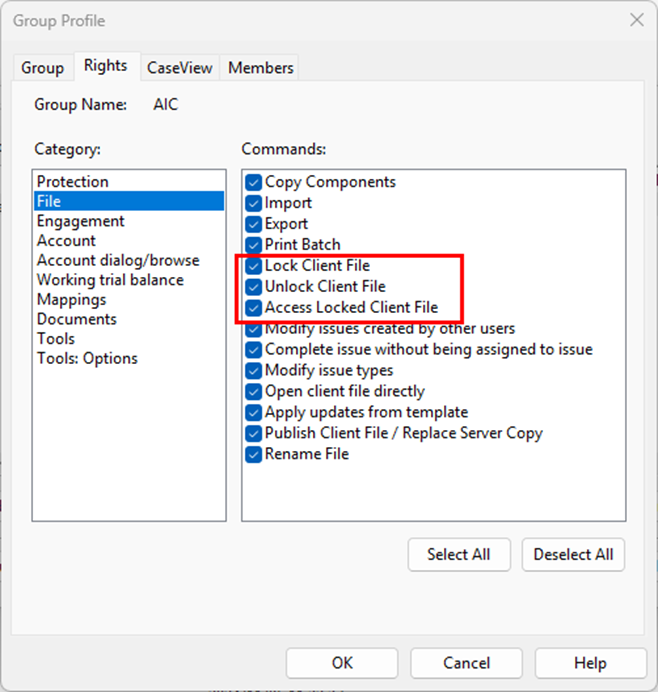

2.1.2. Protection setup

- Split the Lock Client File/Unlock Client File group right into separate Lock Client File and Unlock Client File rights to provide more control over these operations.

2.1.3. Licencing

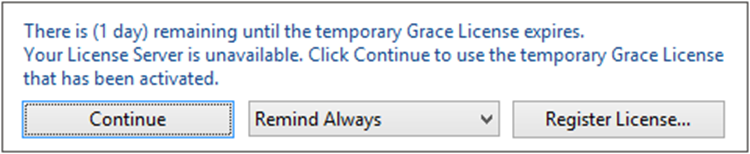

- Added a warning dialog that displays when a Working Papers license is nearing its expiration date.

2.1.4. Hybrid Cloud

- Increased the duration that Working Papers will attempt to communicate with Cloud to prevent the process from timing out before completion.

2.1.5. XBRL

- CaseView now supports multiple XBRL entry points. In the new Select Entry Points dialog, you can add taxonomies and select the applicable entry points to use from the list.

2.2. Improvements

- Attempting to access a computer’s system drive through Caseview causes Caseview to close unexpectedly.

- After performing a silent installation to a newer version of Working Papers, the older version is uninstalled, but the shortcut folder remains in the Windows 10 Start menu.

2.3. Improvements

2.3.1. Imports

2.3.2. SmartSync

-

Documents locked for exclusive use may not indicate that they are ‘Locked’ when opened by the exclusive user, or ‘Read-only’ when opened by other users. The locked/read-only status were still applied, however.

2.3.3. Licencing

2.3.4. XBRL

2.3.5. User Interface

3.1. IPSAS 41 (read together with IPSAS 1, IPSAS 29 and IPSAS 30)

As IPSAS 41 is based on IFRS 9 from a standard development point of view, our development follows the layout utilised in our IFRS Financial Statements product and therefore build on best practices in private sector financial reporting, while ensuring the unique features of the public sector are addressed.

3.1.1. Statement of Financial Position (BS)

The following new line items have been added to the Statement of Financial Position:

Non-current assets:

-

Loans receivable (at amortised cost)

-

Investments at fair value

-

Derivatives

-

Debt instruments at fair value through net assets/equity

-

Receivables from exchange transactions

-

Receivables from non-exchange transactions

Current assets:

- Loans receivable (at amortised cost)

- Investments at fair value

- Derivatives

- Debt instruments at fair value through net assets/equity

Non-current liabilities:

- Derivatives

- Financial liabilities at fair value

- Borrowings

- Financial guarantee contracts

Current liabilities:

- Derivatives

- Financial liabilities at fair value

- Borrowings

- Financial guarantee contracts

The following line items have been removed from the Statement of Financial Position

Non-current assets:

Current assets:

Non-current liabilities:

- Other financial liabilities

Current liabilities:

- Other financial liabilities

3.1.2. Statement of Financial Performance (IS)

The following new line items have been added to the Statement of Financial Performance:

- Gains (losses) on derecognition of financial assets measured at amortised cost

- Gains (losses) on reclassification adjustments from amortised cost to fair value through surplus or deficit

- Gains (losses) on reclassification adjustments from fair value through net assets to fair value through surplus or deficit

The following new line items have removed from the Statement of Financial Performance:

- Gains (Losses) on biological assets and agricultural produce (this line is now part of Gains (Losses) on disposal of asset and liabilities

3.1.3. Statement of Changes in Net Assets (EQ)

The following amendments were made to the Statement of Changes in Net Assets:

- Rename Hedging Reserve to Cashflow Hedging Reserve. Also extended mapping for this section that’s all roles up into this section.

- Rename Fair value adjustments available for sale reserve to Reserve for valuation of financial instruments.

- Added new rows to the Statement of Changes in Net Assets:

- Transfer of cash flow hedging gains (losses) and deferred cost of hedging to the initial carrying amount of the hedged items

- Transfer of credit risk reserve upon derecognition of the related financial liability

- Transfer of investment revaluation reserve upon disposal of investments in equity instruments designated at fair value through net assets/equity

- Loss allowance recognised for debt investments at fair value through net assets/equity

3.1.4. Cashflow Statement (CF) and Cashflow from operations note (CFNOTES_1)

The following new line items have been added to the Cashflow Statement:

Cashflow from investing activities:

- Net movement in loans receivable (at amortised cost)

- Cash advanced in loans receivable (at amortised cost)

- Cash receipts on repayments of loans receivable (at amortised cost)

- Net movement on investments at fair value

- Purchases of investments at fair value

- Proceeds from sales of investments at fair value

- Net movement on debt instruments at fair value through net assets

- Cash advanced on debt instruments at fair value through net assets

- Cash receipts on debt instruments at fair value through net assets

- Cash inflows (outflows) on derivatives

Cashflow from financial activities:

- Net movements on borrowings

- Cash advances received on borrowings

- Cash advances received on borrowings

- Cash inflows (outflows) on derivatives

- Net movements on financial liabilities at fair value

- Repayments of financial liabilities at fair value

- Cash advances received on financial liabilities at fair value

- Cash flows on financial guarantee contracts

Cashflow from operating activities note:

- Derecognition gains on financial assets at amortised cost

- Gains on reclassification of financial assets from amortised cost to fair value through surplus or deficit

- Gains on reclassification of financial assets from fair value through net assets to fair value through surplus or deficit

The following line items have been removed from the Cashflow Statement:

Cashflow from investing activities:

- Net movement in financial assets

- Purchase of financial assets

- Proceeds from sale of financial assets

- Net movement on investments at fair value

Cashflow from financial activities:

- Net movement on other financial liabilities

- Proceeds from other financial liabilities

- Repayment of other financial liabilities

3.1.5. Accounting policies (ACP)

The following accounting policies have been updated:

- Financial instruments (ACP_008)

- Significant estimates and judgements (ACP_000)

3.1.6. Notes to the financial statements (NOTES)

The following new notes have been added:

- Loans receivable (at amortised cost) (NOTES_008)

- Investments at fair value (NOTES_023)

- Derivatives (NOTES_024)

- Debt instruments at fair value through net assets (NOTES_052)

- Borrowings (NOTES_051)

- Financial liabilities at fair value (NOTES_050)

- Financial guarantee contracts (NOTES_071)

- Loans from economic entities (NOTES_048) (previous part of Loans to economic entities, but now separate note)

- Loans from shareholders (NOTES_049) ) (previous part of Loans to shareholders, but now separate note)

- Gains and losses on foreign exchange (NOTES_244)

- Gains (losses) on reclassification of financial assets (NOTES_249)

- Derecognition gains on financial assets at amortised cost (NOTES_246)

- Financial instrument and risk management (NOTES_211)

The following notes have been updated:

- Loans to economic entities (NOTES_009)

- Loans to shareholders (NOTES_010)

- Loans to directors, managers and employees (NOTES_017)

- Cash and cash equivalents (NOTES_019)

- Receivables from exchange transactions (NOTES_016)

- Receivables from non-exchange transactions (NOTES_209)

- Payables exchange (NOTES_033)

- Taxes and transfers payable (non-exchange) (NOTES_210)

- Gains on disposal of assets (NOTES_226)

- Fair value adjustments (NOTES_123)

- Impairment (NOTES_130)

- Dividends received (NOTES_222)

- Interest received - Investment (NOTES_225)

- Finance costs (NOTES_125)

- Foreign currency translation reservice (NOTES_063)

- Hedging reserve (NOTES_064)

- Reserve for valuation of investments (NOTES_066)

The following notes have been removed:

- Other financial assets (NOTES_011)

- Other financial liabilities (NOTES_028)

- Financial instruments disclosure (NOTES_218)

3.1.7. Statement of Comparison of Budget and Actual amounts (BC)

This statement has been updated to align to the Statement of Financial Performance, Statement of Financial Position and Statement of Changes in Net Assets.

3.1.8. Document manager

Added the following new leadsheets on the document manager:

- 340 Loans receivable

- 341 Debt instruments at FV through net assets/equity

- 351 Investments at fair value

- 352 Derivatives

- 547 Loans from economic entities

- 548 Loans from shareholders

- 550 Financial liabilities at fair value

- 551 Borrowings

- 553 Financial guarantee contracts

- 560 Social benefits liabilities

Added the following leadsheets have been renamed from the document manager:

- 550 Renamed to "Financial liabilities at fair value"

Added the following leadsheets have been removed from the document manager:

- 350 Other financial assets

3.2. IPSAS 42 - Social Benefits

The following sections have been updated for due to IPSAS 42 - Social Benefits:

- Statement of Financial Position:

- Add new line for Social Benefits under current and non current liabilities (BS)

- Statement of Financial Performance

- Add new line for Social Benefit expenses (IS)

- Cash flow statement (CF)

- Add a new line for Social Benefit expenses under operating activities

- Add new line for Social Benefits under current and non current liabilities (BS)

- Statement of Comparison of budget and actual amounts (BC)

- Add a new row for Social Benefit expenses in the Statement of Financial Performance section

- Add a new row for Social Benefits liability in the Statement of financial Position section

- Add a new row for Social Benefit expense on the Cashflow from operational activities section

- Add a new row for Social Benefit liability in the Cashflow from finance activities section

- Accounting policies

- Add a new accounting policy for Social Benefits (ACP_007)

- Notes to the financial statements

- Add a new note for Social Benefit liabilities (NOTES_106)

- Update the Provision note to remove references to Social Benefit liabilities (NOTES_031)

- Document manager

- Add new leadsheet 560 for Social Benefits

3.3. Other compliance changes

The following sections have been updated for due minor compliance changes from amendments to existing standards:

- Update the accounting policy for Provisions (IPSAS 19) for Collective and individual services. (NOTES_031)

- Update the New Standards and Interpretations note for reference to IPSAS 49 Retirement Benefit Plans and Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities. (NOTES_047)

- Added a new note for " Changes in liabilities arising from financing activities" as required by IPSAS 2 - Cashflow statement. (NOTES_176)

- Update the accounting policy for " Service concession arrangements: Grantor". (ACP_068)

- Change the mapping range for Service concession arrangements from 1.5.?.450 to 1.5.?.209. This required an update of mapping reference for the note for Service concession arrangements, cashflow statement and statement of comparison of budget and actuals amounts. (NOTES_104)

3.4. Alignment to Kenya specimen

The following sections have been updated to align to the Kenya specimen:

- The Board of Directors/Council. (OR1)

- Key Management Team (OR5)

- Appendix 1 - SFPer for each quarter.

3.5. Other user request improvements

Other than compliance the following user request improvements are added in this update:

- Added the ability to have two logos on the cover page.

- Added a new alpha numeric table in the super insert option for tables.

- Improve the speed of the super insert option.

4. Previous release - Caseware Working Papers 2024.00.092

The following describes the features and fixes included in Working Papers 2024 and related products.

4.1. Features

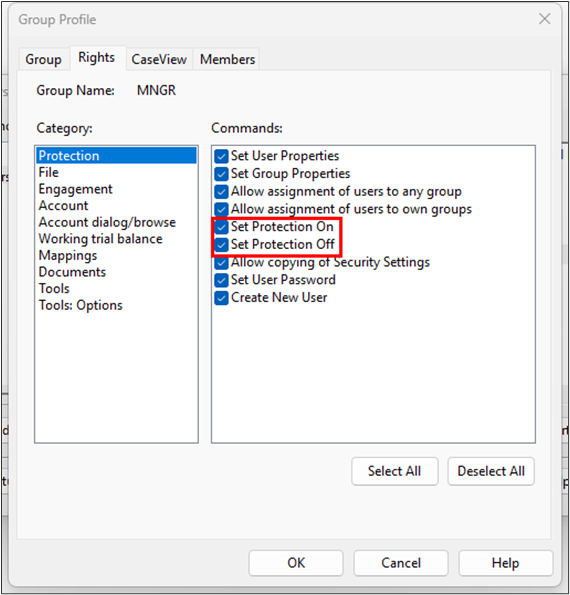

4.1.1. Protection setup

Split the existing Set Protection On/Off group right into Set Protection On and Set Protection Off. This can be used to expand the number of users that can enable file protection without giving them the ability to disable it.

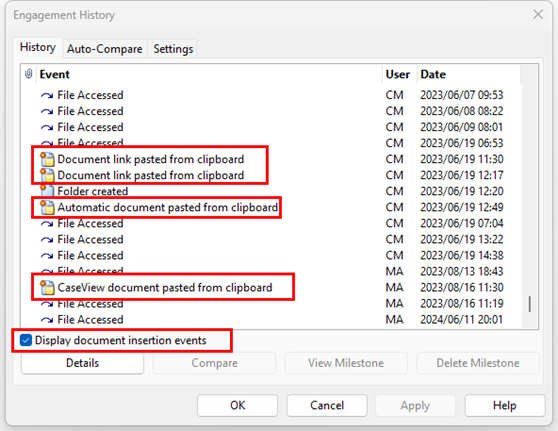

4.1.2. History and milestones

Added an option to display document insertion events in the file history log.

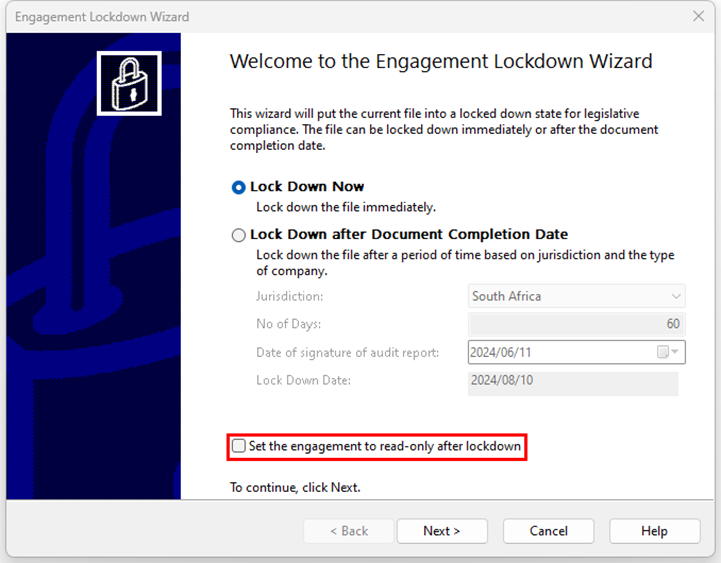

4.1.3. Lockdowns

Added an option to the Engagement Lockdown Wizard to set all content in a file’s directory to read-only after lockdown. This read-only mode also applies to any sync copies of the file.

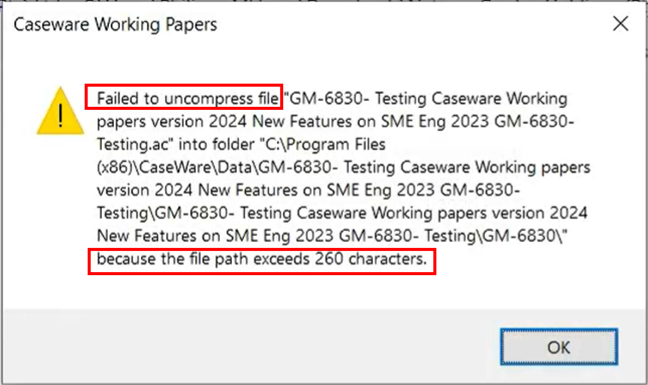

4.1.4. More informative Error Messaging

Added a more informative error dialog when attempting to open a compressed file that contains documents with file paths exceeding 260 characters.

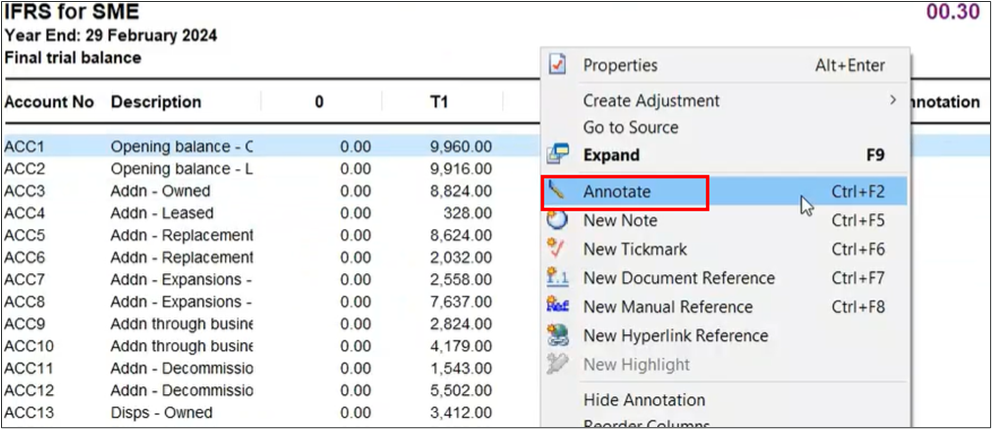

4.1.5. Annotations

The Annotation column is now visible in trial balance automatic documents using the Consolidated view.

4.1.6. Caseview scripting

Increased the character limit for CaseView script names to 31 characters. This increased character limit aligns with the existing CaseView UI limit and prevents some potential scripting errors.

4.1.7. Data Store Administration Tool

The Data Store Administration Tool (DSAT) can now be used with Microsoft SQL Server 2022.

4.1.8. Imports and exports

- Added support for imports from the following software packages:

- QuickBooks 2024 (Australia, Canada, UK)

- Sage 50 Accounting 2024 (Canada)

- Added support for exports to the following software packages:

- ProFile 2023 (Canada)

- The import process for QuickBooks US files now matches the process to import QuickBooks Canada, UK and Australia files. This process requires the QuickBooks Export Utility.

4.2. Improvement

- When importing a trial balance with map numbers, nonexistent map numbers will not be created. This reduces the risk of assigning accounts to map numbers which are not catered for in the rest of the product.

- Attempting to access a computer’s system drive through CaseView causes CaseView to close unexpectedly.

- After performing a silent installation to a newer version of Working Papers, the older version is uninstalled, but the shortcut folder remains in the Windows 10 Start menu.

The IPSAS template share the same system requirements as Caseware Working Papers. Click here to view the system requirements

Kindly find all the information you need on our previous release:

Rate this article: